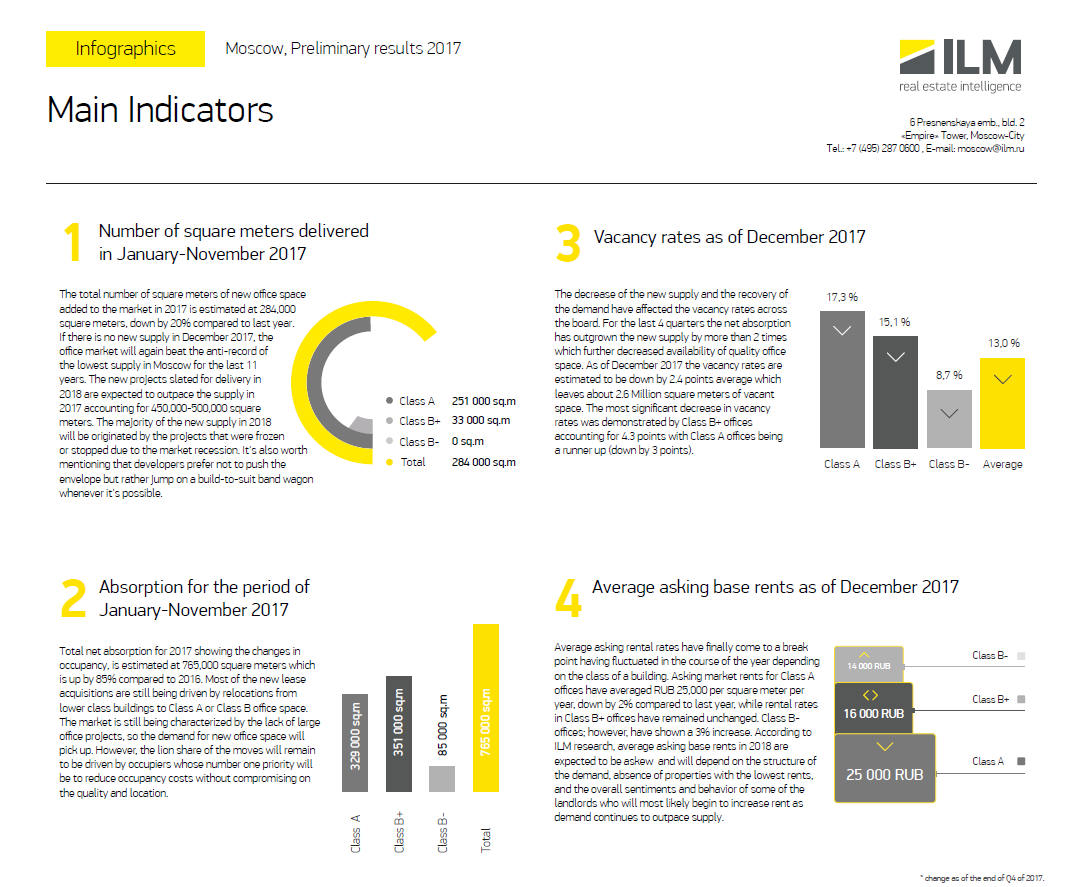

Number of square meters delivered in Jan-Nov. 2017

- Class A

- Class B

- Class B-

- Total

- 251000 м²

- 33000 м²

- 0 м²

- 284000 м²

According to preliminary results, during the year 284 thousand square meters of office space were commissioned, which is 20% less than the volume of new construction last year.

In case there will be no more new facilities until the end of the year, the indicator will again update the “anti-record” among similar

values of the past 11 years in the Moscow office real estate market.

The volume of projects under construction, the commissioning of which is scheduled for 2018, may grow relative to the current year and will be about 450-500 thousand square meters. And the overall increase in expected areas in the next year will be formed mostly from objects with deferred or postponed readiness. It should be noted that a large number of objects appear on the market, the construction of which can be completed for a specific client.

Absorption for Jan-Nov. 2017

The total net absorption of the four quarters, showing the change in office space occupied by tenants, according to preliminary data amounted to 765 thousand square meters, exceeding last year's value by 85%. From the structure of the total net absorption, it can be seen that the demand for new office space is still largely formed by moving companies to high-end facilities. Taking into account the shortage of large areas and the lack of new offers, the activity of tenants in the office segment will increase. At the same time, the relocation of most companies will continue to be driven by the desire to optimize rental costs.

Vacancy rates as of the end of December 2017

The decrease in the volume of new construction and the restoration of stable demand had an impact on reducing the share of unclaimed premises. Over the past four quarters, net absorption exceeded the volume of new construction by more than two times, which led to a further reduction in the level of unclaimed premises. Compared with the end of last year, the vacancy rate according to preliminary results decreased by 2.9 percentage points. and amounted to 12.9%. Thus, at the moment, 2.6 million square meters of office space remain unoccupied. The largest decrease in the indicator was recorded in class B + objects. Due to the increase in net absorption, the share of vacant premises here has decreased by 4.3 pp compared to the beginning of the year. In class A, the decline was 3 percentage points.

Average asking base rates as of the end of December 2017

14000 rub.

14000 rub. 16000 rub.

16000 rub. 25000 rub.

25000 rub.During the year, the average requested base rental rates stabilized. Compared to the end of 2016, the average rental rate has undergone some fluctuations depending on the class.

In class A objects, the average level of requested rental rates in ruble equivalent according to preliminary results reached 25,000 rubles. for the sq. m. per year, which is 2% lower compared to the end of last year. In class B + ruble rental rates remained at the same level. In class B, rates increased by 3%. According to our expectations, the average level of rental rates next year may fluctuate depending on the adjustment of the supply structure and withdrawal from the market of cheap offers, as well as on the behavior of individual owners, some of which will gradually increase the rental price against the background of stabilization.

Год

Год